PORTAL

PORTAL

Home

Home Analytics (2) 14.07.26

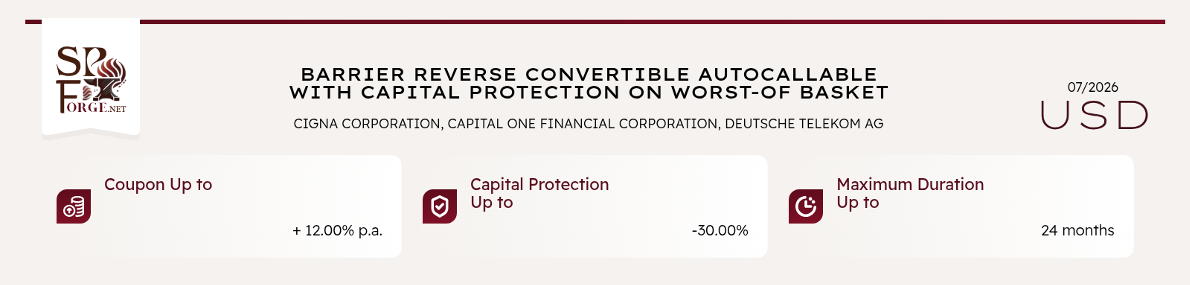

After a turbulent first half of 2026, several solid companies are trading below levels supported by their fundamentals. We selected stocks that posted negative returns in the first half of 2026 despite strong financials and high analyst “buy” ratings. The basket includes two US companies and one German company from reliable sectors: Telecommunications, Financials and Health Care. We see all three as undervalued and unlikely to fall below the 70% capital protection barrier over the two-year term, while offering a double-digit annual coupon.

The Cigna Group [Internal score 91/100] is a US healthcare and insurance company operating in more than 30 countries with over 190 million customer relationships. It delivers care through two main divisions: Cigna Healthcare (40% of earnings) and Evernorth Health Services (60% of earnings). Since 2014, adjusted EPS has grown by 14% per year, from $7.87 to $27.30. In the 1st quarter of 2026, revenue rose 4.6% y/y to more than $68.4B, while net income increased 13% to $1.7B. Cigna has generated positive FCF for more than ten years, including $864 million in the latest quarter. Evernorth recently announced Pharmacy Forward, an AI-enabled specialty pharmacy platform backed by a $100 million investment through 2028. The company expects it to create around $400 million in value by the end of 2028.

Deutsche Telekom [Internal score 73/100] is a partly state-owned German company and Europe’s largest telecom provider by revenue. It owns just over 50% of T-Mobile US, which generated 66% of adjusted EBITDA in the 1st quarter. Germany contributed 23%, while other EU markets accounted for 10%. In the 1st quarter, organic service revenue outside the US rose 2.2%, while adjusted EBITDA increased 2.5%. Revenue grew 0.4% y/y to €29.9B, and net income exceeded €2.7B. The group has 273 million mobile subscribers, 24 million fixed-line customers and more than 22 million internet users. Deutsche Telekom is also working with Starlink to expand hybrid terrestrial and satellite connectivity. During the 1st quarter, S&P upgraded its credit rating from BBB+ to A-.

Capital One Financial Corp [Internal score 65/100] is a major US bank holding company and the country’s largest credit card issuer. It also operates in consumer and commercial banking, auto finance and investment banking through Capital One Securities. In the 1st quarter of 2026, total assets exceeded $682.9B, with $447.9B in loans and $489B in deposits. Net revenue reached $15.2B, up 52.3% y/y, while net income rose to $2.8B, almost double the the 1st quarter of 2025 level. Net interest income increased from $8.0B in the 1st quarter of 2025 to $12.1B, while the net interest margin rose from 6.93% to 7.87%. Credit cards generate 76% of total NII, followed by Consumer Banking at 18%, Commercial Banking at 5% and other activities at 1%.

Several near-term events could bring attention back to the basket. Capital One reports Q2 results on 21 July, followed by Cigna on 30 July and Deutsche Telekom on 6 August. Strong earnings and stable guidance could show that the recent price weakness is not driven by weaker fundamentals. The Fed meeting on 28–29 July is another catalyst: higher-for-longer rates would support Capital One’s interest income, while a softer signal could reduce funding and credit pressure and support valuations across the basket.